Job creation exceeded expectations in February, but the unemployment rate rose and employment growth compared to the previous two months was not as great as initially reported.

The Labor Department's Bureau of Labor Statistics reported Friday that nonfarm payrolls increased by 275,000 during the month while the unemployment rate rose to 3.9%. Economists surveyed by Dow Jones were looking for payroll growth of 198,000.

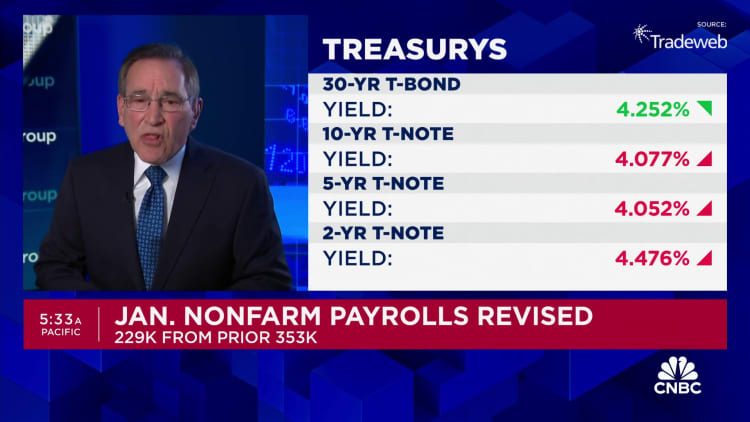

February was a step higher in growth than January, which saw a sharp downward revision to 229,000, from the 353,000 initially reported. Job growth in December was also revised to 290,000 from 333,000, bringing the two-month payrolls total to 167,000 fewer than initially reported.

The level of unemployment rose as the Household Survey, used to calculate the unemployment rate, showed a decrease of 184,000 in the number of workers. This increase came despite the labor force participation rate remaining stable at 62.5%, despite the rise in the “basic age” rate to 83.5%, an increase of twenty percentage points. The establishments survey shows the total number of jobs.

Average hourly earnings, which are closely watched as an indicator of inflation, showed a slightly smaller-than-expected increase for this month and a slowdown from last year. Wages rose just 0.1% month over month, a tenth of a percentage point below estimates, and were up 4.3% from a year ago, down from the 4.5% increase in January and just below the 4.4% estimate.

Hours worked rebounded from a decline in January, with the average work week rising to 34.3 hours, an increase of 0.1 percentage point.

Jobs numbers are likely to keep the Federal Reserve on track to cut interest rates later this year, although the timing and extent remain uncertain.

Stocks rose on Friday following the news, with the Dow Jones Industrial Average rising about 150 points in early trading. Treasury yields fell. Indicator 10 year note The latter was at 4.07%, down about 0.02 percentage points during the session.

“It literally has a data point for every viewpoint on the spectrum,” Liz Ann Saunders, chief investment strategist at Charles Schwab, said of the report. These range from “the economy is sliding into recession to moderate, all is well, nothing to see here. It's definitely mixed,” she added.

Job creation is skewed towards part-time jobs. Full-time employment fell by 187,000 while part-time employment rose by 51,000, according to the household survey. An alternative measure of unemployment, sometimes called the “true” unemployment rate, which includes discouraged workers and those working part-time jobs for economic reasons, rose slightly to 7.3%.

From a sector perspective, healthcare led with 67,000 new jobs. The government was again a big contributor, with 52,000, while restaurants and bars added 42,000 and social assistance increased by 24,000. Other gainers included construction (23,000), transportation and warehousing (20,000) and retail (19,000).

The report comes with markets on edge over the state of growth in the broader economy and the impact it may have on monetary policy. Futures trading moved slightly following the report, with traders now pricing in greater certainty over the Fed's initial interest rate cut in June.

“There's nothing new under the sun between this report and last month's report. It doesn't give us a lot of information, other than what we can say qualitatively, we're still growing jobs at a good pace and wages are still high.” “A little higher than we would like,” said Dan North, chief economist at Allianz Trade Americas.

North added that the report probably “doesn't change the narrative” for the Fed, although he believes the first cut may not happen until July.

In recent days, Fed officials have sent mixed signals, suggesting that inflation is cooling but not enough to warrant the first interest rate cuts since the early days of the Covid pandemic crisis.

Federal Reserve Chairman Jerome Powell, speaking this week on Capitol Hill, described the labor market as “relatively tight” but moving toward a better balance than the days when job openings outnumbered available workers by a 2-to-1 margin.

Besides, he said inflation has “declined significantly” although it still does not show enough progress to return to the Fed’s 2% target. But he told the Senate Banking Committee on Thursday that the state of the economy is such that the Fed is “not far off” from when it can start easing monetary policy.

“We have a data-driven database, which means we are all at the mercy of the data,” Saunders said. “Big moves outside of consensus on labor market data, inflation data, can move the needle. But numbers that are consistent or mixed, we all move on to the next report.”

Job creation has remained strong despite a wave of high-profile layoffs, especially in the technology industry. Recently, companies such as Cisco, Microsoft, and SAP have announced significant reductions in their workforces. Outsourcing firm Challenger, Gray & Christmas said this February was the worst month for layoff announcements since 2009, in the late days of the global financial crisis.

However, it appears that workers are still able to find work. Job openings were virtually unchanged in January at nearly 9 million and still outnumbered the unemployed by a ratio of 1.4 to 1. Weekly unemployment claims moved little, at 217,000 in the final week of filings, although continuing claims topped 1.9 million. Only, the four-week moving average for this measure reached its highest level since December 2021.

Amid mixed signals, markets trimmed their expectations for a rate cut from the Federal Reserve. Futures market traders are pricing in the first cut coming in June, versus March expectations at the start of the year, and now expect four total cuts this year versus six or seven previously, according to CME Group data.