Sergio Ermotti, CEO of Swiss banking giant UBS, during the group's annual shareholders meeting in Zurich on May 2, 2013.

Fabrice Coffrini | AFP | Getty Images

Switzerland's strict new banking regulations create a 'lose-lose situation'. UPS It may limit its ability to challenge Wall Street giants, according to Beate Wittmann, a partner at Zurich-based Porta Advisors.

In a 209-page plan published on Wednesday, the Swiss government proposed 22 measures aimed at tightening supervision over banks deemed “too big to fail,” a year after authorities were forced to mediate an emergency rescue of Credit Suisse by… “UPS”.

The government-backed takeover was the largest merger between two systemically important banks since the global financial crisis.

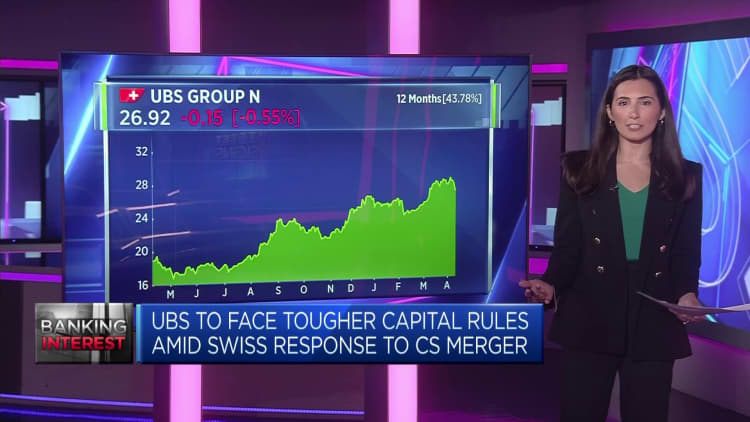

At $1.7 trillion, UBS's balance sheet is now double the country's annual gross domestic product, which has heightened scrutiny of protectionist measures surrounding the Swiss banking sector and the broader economy in the wake of the collapse of Credit Suisse.

Speaking on CNBC's “Squawk Box Europe” on Thursday, Whitman said Credit Suisse's downfall was “a completely self-inflicted and predictable failure of policy by the government, the central bank and the regulator, above all else.” [of the] Minister of Finance.”

“Then of course Credit Suisse had a failed, unsustainable business model and incompetent leadership, all of which was indicated by the continued decline in equity prices and credit spreads throughout [20]22, [which was] “It has been completely ignored because there is no institutional knowledge at policy maker levels to monitor capital markets, which is essential in the case of the banking sector,” he added.

A report released on Wednesday grants additional powers to the Swiss Financial Market Supervisory Authority, introduces capital surcharges and strengthens the financial position of subsidiaries – but stops short of recommending a “comprehensive increase” in capital requirements.

Whitman noted that the report does nothing to allay concerns about the ability of politicians and regulators to supervise banks while ensuring their global competitiveness, saying that it “creates a situation in which everyone loses Switzerland as a financial center and UBS will not be able to develop its business.” Possible.”

Regulatory reform must take priority over tightening the screws on the country's biggest banks, he said, if UBS is to capitalize on its new scale and finally challenge its ilk. Goldman Sachs, JP Morgan, Citigroup And Morgan Stanley – which have balance sheets of similar size, but trade at a much higher valuation.

“It's about the regulatory level,” Whitman said. “It's about competencies, of course, and then the incentives and the regulatory framework, and the regulatory framework like capital requirements is a global practice.”

“Switzerland or any other jurisdiction can't impose very different rules and levels there – it doesn't make any sense, so you can't really compete.”

For UBS to improve its capabilities, Whitman said the Swiss regulatory system must be aligned with that in Frankfurt, London and New York, but he said Wednesday's report showed an “unwillingness to engage in any relevant reforms” that would protect banks. The Swiss economy and taxpayers, but it enables UBS to “catch up with global players and US valuations”.

“The track record of Swiss policymakers is that we had three global banks relevant to the financial system, and now we have one bank left, and these cases were a direct result of inadequate regulation and enforcement,” he said.

“FINMA had all the legal background and tools in place to address the situation but they did not implement them – that is the point – and now we are talking about fines, that seems foolish to me.”