In the case of societal and private nonprofit education, California’s household use high amounts however, appear to compensate for they having cost activities that bring all of them nearer to the fresh new national mean. Source: Author’s research of data on University Scorecard organization-level dataset, through the U.S. Agency off Training. Discover Shape 37 regarding partner statement . “> 65 (Look for Contour 10.) Less so for Father or mother Plus money borrowed getting to have-funds knowledge; among parents one to lent Mother or father Plus to own a concerning-earnings college or university, the average loan harmony is actually forty five per cent high during the Ca than the remainder You among parents that had been from inside the fees for one year, and you will 56 per cent to own parents that were in the cost to own five years. Ibid. “> 66

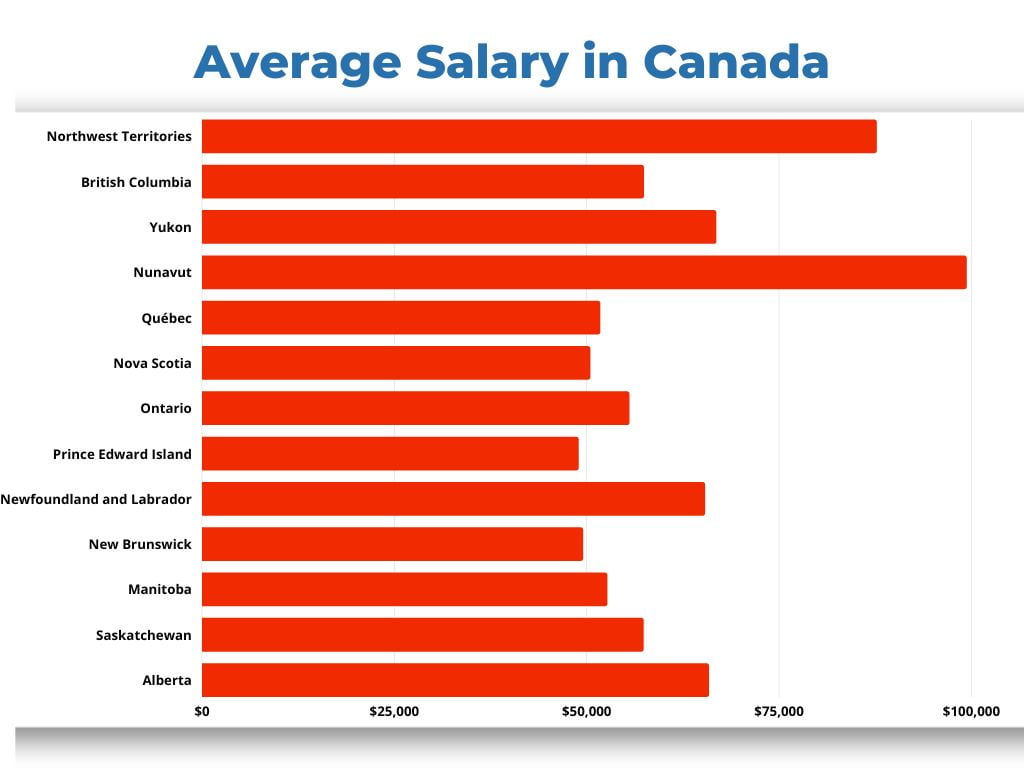

Profile 10

Its notable and you can surprising that Ca was a standout instance out-of highest financial obligation burdens for attending to own-earnings, considering the less expensive solutions in order to California’s family members through its condition educational funding and you may neighborhood educational costs waivers. Such habits along with show how borrowing from the bank to go to to have-profits can be adversely affect the mothers of your youngsters one to sit-in them, not merely the young who enter.

Graduate Fund

A graduate-height degree, such as for example a master’s or doctoral studies, draws we trying to progress inside their field. Heightened event about employees work for people, but policymakers have to grapple for the long-label economic effects of these debt for household in addition to brand new different affects by battle and you will class record.

Because of the full loan amount, graduate pupils are many yearly borrowing inside the California, place Ca one of one of merely three states (as well as Puerto Rico and you will Washington, D.C.) where scholar loan applications lead over fifty percent of all financing cash paid per year. Ibid. “> 71

In this California’s scholar obligations, concerning the trend arise. One of to have-earnings colleges, the common yearly Grad In addition to mortgage from inside the Ca are $31,600, that is 43 percent more the common one of getting-winnings throughout the remaining portion of the All of us. Source: author’s data of information regarding the Federal College student Services Investigation Heart. Look for Figure 1 in the fresh partner declaration . “> 72 Certainly one of individual nonprofit colleges, annual Graduate Together with loans is highest, averaging $33,2 hundred annually for the California, but the gap between California together with other countries in the United Claims is significantly smaller (11 per cent). Merely from the to own-finances industry manage Stafford graduate finance during the California surpass those in the remainder All of us of the an important margin, on twenty seven percent.

Table step 3

On cohort out of borrowers have been inside the cost to own 5 years towards a scholar mortgage away from a concerning-finances college, California borrowers’ mediocre financing equilibrium is $81,600 bad credit personal loans West Virginia, that is more than twice as much mediocre to your to own-money cohort throughout the remaining portion of the Us.

Figure 11

Analysis toward attainment and you may income make sure the official benefit places a premium on the postsecondary studies, highlighting a savings very stratified according to workers’ education membership:

A cost savings designated by the such as inequality helps make men be such as climbing up the brand new hierarchy is worth people costs. Enter As well as money, that indeed security people pricing if your borrower lets all of them.

Regrettably, not totally all which follow a diploma sooner or later receive high revenues, and could possibly get challenge into the payment. Graduate And financing are eligible to have income-driven repayment (IDR), the fresh new federal student loan repayment bundle which is most amenable to help you consumers that have low income. Becoming more California consumers towards IDR plans is actually a state consideration in depth about CSAC Education loan and Debt Services Review Workgroup’s latest declaration, and Grad And additionally individuals particularly perform make the most of IDR. But not, Mother Including isnt eligible for IDR, while making such financing especially harmful getting mothers versus solid money. Moms and dad Along with loans pose a really thorny public plan material, because the state lawmakers don’t turn-to the techniques from signing up even more moms and dad-borrowers on the IDR.